The Two Layers of Nonprofit Law: What Founders Should Know About Federal vs. State Oversight

Follow the Mt. Frissell Trail about two miles into the northwestern-most point of Connecticut, and you will find a stone pillar placed in 1898. The Connecticut-Massachusetts-New York Tri-State Monument marks the boundaries where the three states converge. Imagine walking in a circle around that monument as a nonprofit organization. In the eyes of the Federal government, you may be a 501(c)(3). But step into Massachusetts and you are a Public Charity Corporation. Move southwest into New York and you become a Not-for-Profit Corporation. Take a step east and Connecticut recognizes you as a Nonstock Corporation. Each step places you under a different legal regime—with distinct agencies, filings, and compliance obligations.

As we previously learned, Federal oversight of nonprofits focuses on tax-exemption status (usually under one of the 501(c) categories). Federal rules govern eligibility for exemption, requiring annual filings (e.g., IRS Form 990), limit lobbying and political activities, and prohibit private inurement. These standards determine what makes an organization charitable, but they do not dictate most of the governance or structural requirements. This is why formation documents— Articles of Incorporation and Bylaws—must be drafted with both Federal and state requirements in mind. Even after IRS recognition, a nonprofit still faces a second and often more complex layer of state regulation.

States generally impose a common set of compliance obligations (with slight variations in the names), including:

Articles of Incorporation and bylaws,

regular reports,

charitable solicitation registration and renewal, and

financial reporting and audits.

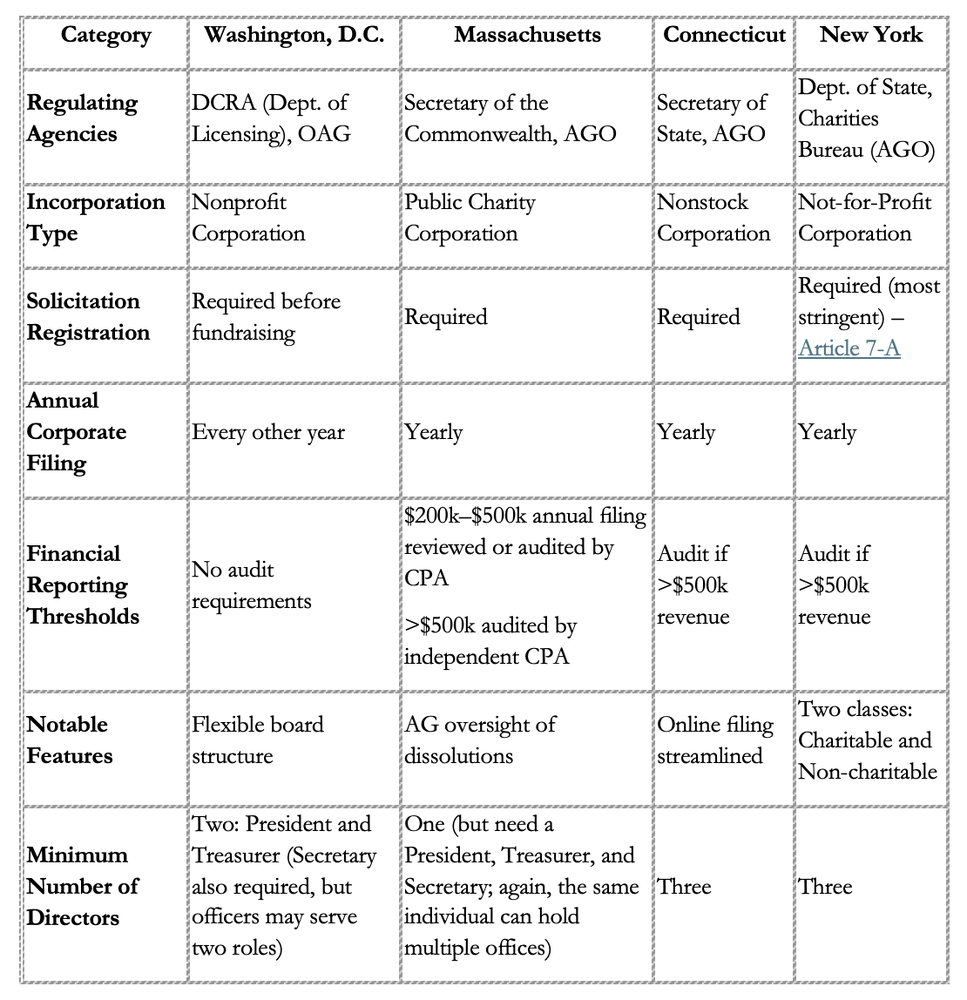

But the details – and timing – of these filings can vary. As examples, we will look briefly at how DC, New York, Massachusetts, and Connecticut regulate tax-exempt corporations:

As the table reflects, New York maintains the most rigorous solicitation oversight (Article 7-A), Massachusetts imposes tiered audit requirements (M.G.L. c. 12 § 8F), and DC permits flexible board structures, such as designating a body with limited board authority (see D.C. Code § 29-406.12). These variations underscore the importance of multi-state compliance for nonprofits that operate or fundraise across state lines.

Importantly, a nonprofit must satisfy state incorporation requirements before applying for Federal exemption and must maintain good standing thereafter. Falling out of good standing can jeopardize Federal status. And IRS exemption alone does not authorize fundraising in any state; separate charitable solicitation registrations are required.

Laws evolve, and they do so independently in each jurisdiction. Nonprofit leaders must not only understand the requirements in each state where they operate but also monitor ongoing legislative and regulatory developments. Compliance protects the organization’s tax-exempt status, fosters donor trust, and promotes ethical, transparent operations. At Commonlight Legal, we monitor these changes daily and support nonprofit leaders with state-specific guidance and compliance reviews.

This article is for general informational purposes only and does not constitute legal advice. Reading this article does not create an attorney-client relationship. For advice specific to your organization's situation, contact Commonlight Legal LLP.